We are seeking your feedback and experiences with the Interim Control Bylaw, currently in effect in the City of Burlington. Below are the details of the bylaw, as well as a link to submit your feedback.

Interim Control Bylaw (ICBL)

On March 5, 2019, Burlington City Council implemented a Temporary Development Freeze (Interim Control Bylaw, or ICBL) within areas of downtown Burlington and surrounding the Burlington GO Station. This Freeze will last one year, with a maximum extension of a second year.

On April 2, 2019, Burlington City Council amended the Temporary Development Freeze to include exemptions – “Building of pools, decks, fences and interior alterations are permitted. These types of developments are considered minor and/or accessory to the main use of the property. They are not considered to affect intensity or land use in the study area, so they are exempt from the ICBL.”

The construction of a new home or an addition to an existing home still fall within the ICBL.

We would appreciate your feedback on this Temporary Development Freeze – specifically if you or your clients have experienced any issues or disadvantages as a result of the Freeze, as well as how you think this Freeze may be affecting property values in Burlington.

To submit your feedback, please click the below button. It should take no longer than two (2) minutes of your time. We ask that you please provide your feedback by Friday, August 2, 2019.

On July 10, 2019, Jean-Yves Duclos, Minister of Families, Children and Social Development, announced the new First-Time Home Buyer Incentive. Below are the details, criteria and conditions of this new Incentive.

Details:

The new Incentive will start in September 2, 2019, with the first closing on November 1, 2019.

The aim of the Incentive is to help middle-class families take the first step towards home ownership.

For the purchase of an existing home, an incentive amount of five per cent may be available.

For the purchase of a newly constructed home, an incentive amount of five per cent or 10 per cent may be available.

This is a shared equity mortgage with the Government of Canada.

The government shares in the upside and downside of the change in the property value.

The total amount of funding will be $1.25 billion over three years.

Criteria:

The incentive will allow eligible first-time home buyers who have the minimum down payment for an insured mortgage with CMHC, Genworth or Canada Guaranty, to apply to finance a portion of their home purchase through a form of shared equity mortgage with the Government of Canada.

The property must be located in Canada and must be suitable and available for full-time, year-round occupancy.

Eligible for Canadian citizens, permanent residents, and non-permanent residents who are legally authorized to work in Canada.

The incentive will be available to first-time home buyers with qualified annual household incomes up to $120,000.

The above-listed income (up to $120,000) is subject to qualifying income requirements set out by lenders and mortgage loan insurers.

At least one borrower must be a first-time home buyer.

DEFINITION: you have never purchased a home before; you have gone through a breakdown of a marriage or common-law partnership (even if you don’t meet the other first-time home buyer requirements); or in the last four years, you did not occupy a home that you or your current spouse or common-law partner owned.

The minimum down payment must come from traditional down payment sources. Traditional down payment comes from the borrower’s own resources and may include:

savings

withdrawal/collapse of a registered retirement savings plan (RRSP)

non-repayable financial gift from a relative

NOTE: Unsecured personal loans or unsecured lines of credit used to satisfy minimum down payment requirements are not eligible for the program.

A participant’s insured mortgage and the incentive amount cannot be greater than four times the participant’s qualified annual household income.

Conditions:

No on-going repayments are required.

The incentive is not interest bearing.

The borrower can repay the Incentive at any time without a pre-payment penalty.

Refinancing of the first mortgage will not trigger repayment.

The Incentive is a second mortgage on the title of the property.

The first mortgage must be greater than 80 per cent of the value of the property and is subject to a mortgage loan insurance premium.

At the present time, the buyer must repay the incentive after 25 years or if the property is sold – whatever comes first.

The repayment of the Incentive is based on the property’s fair market value.

If your property value goes down, you are still responsible for repaying the shared equity mortgage based on the current home value at time of repayment.

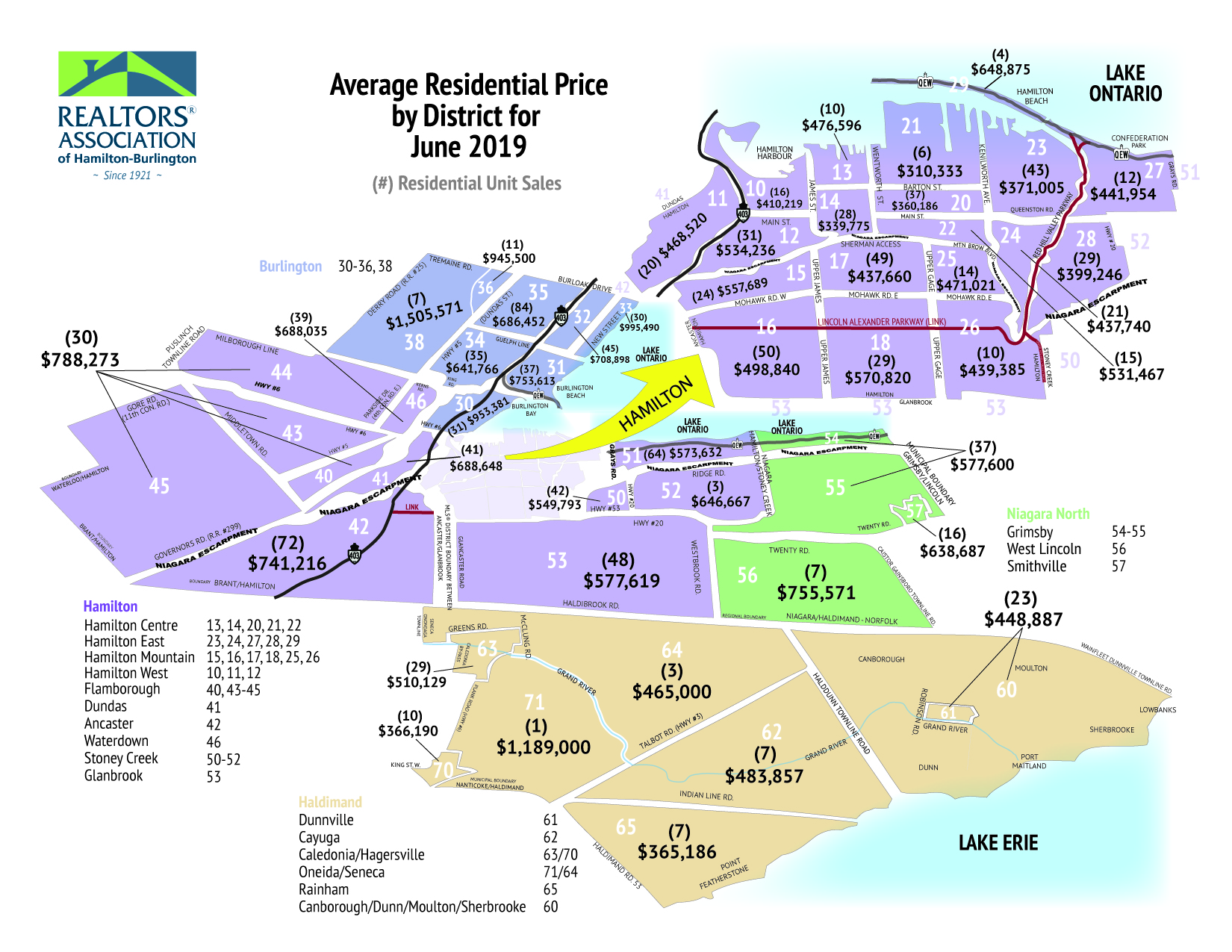

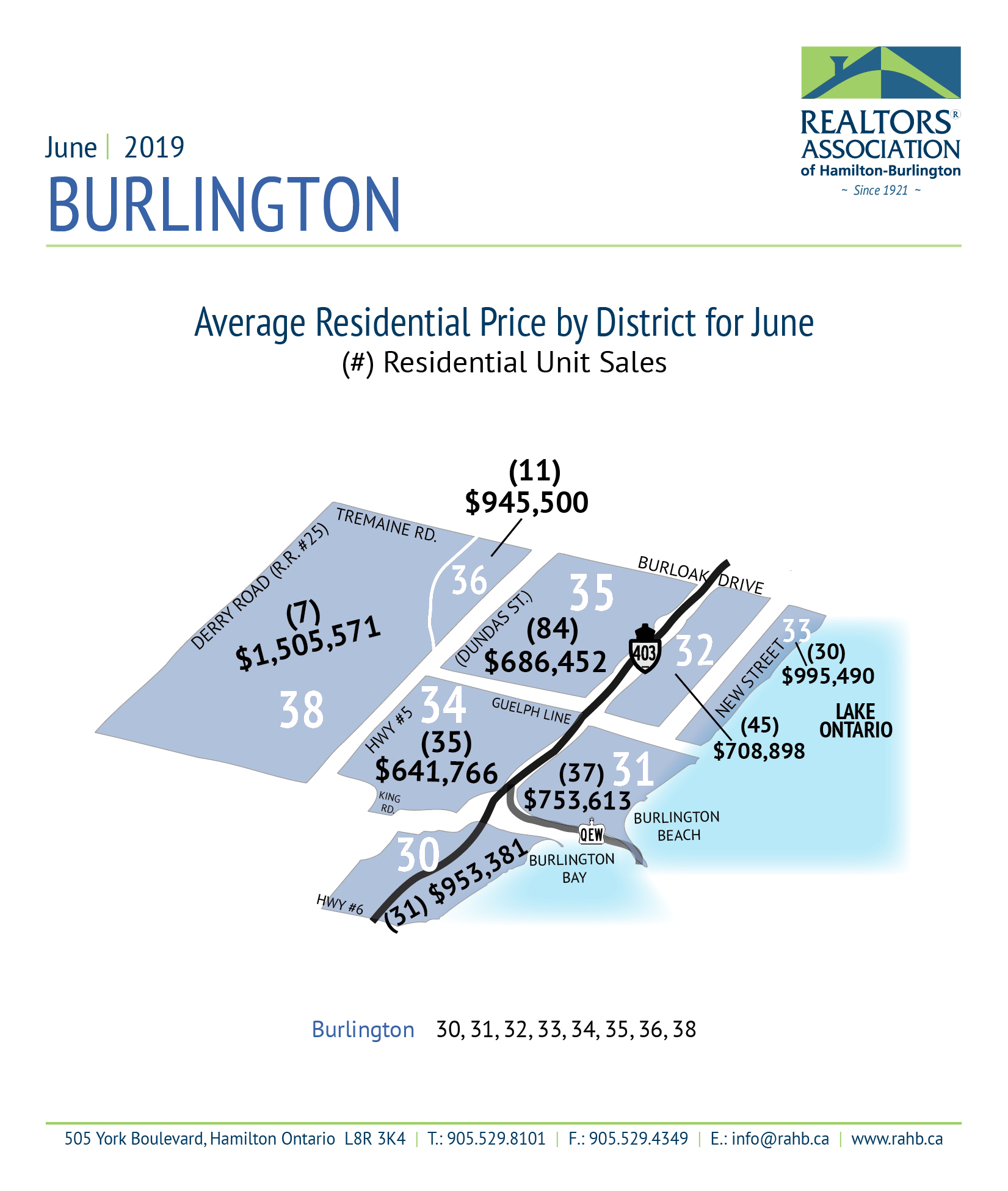

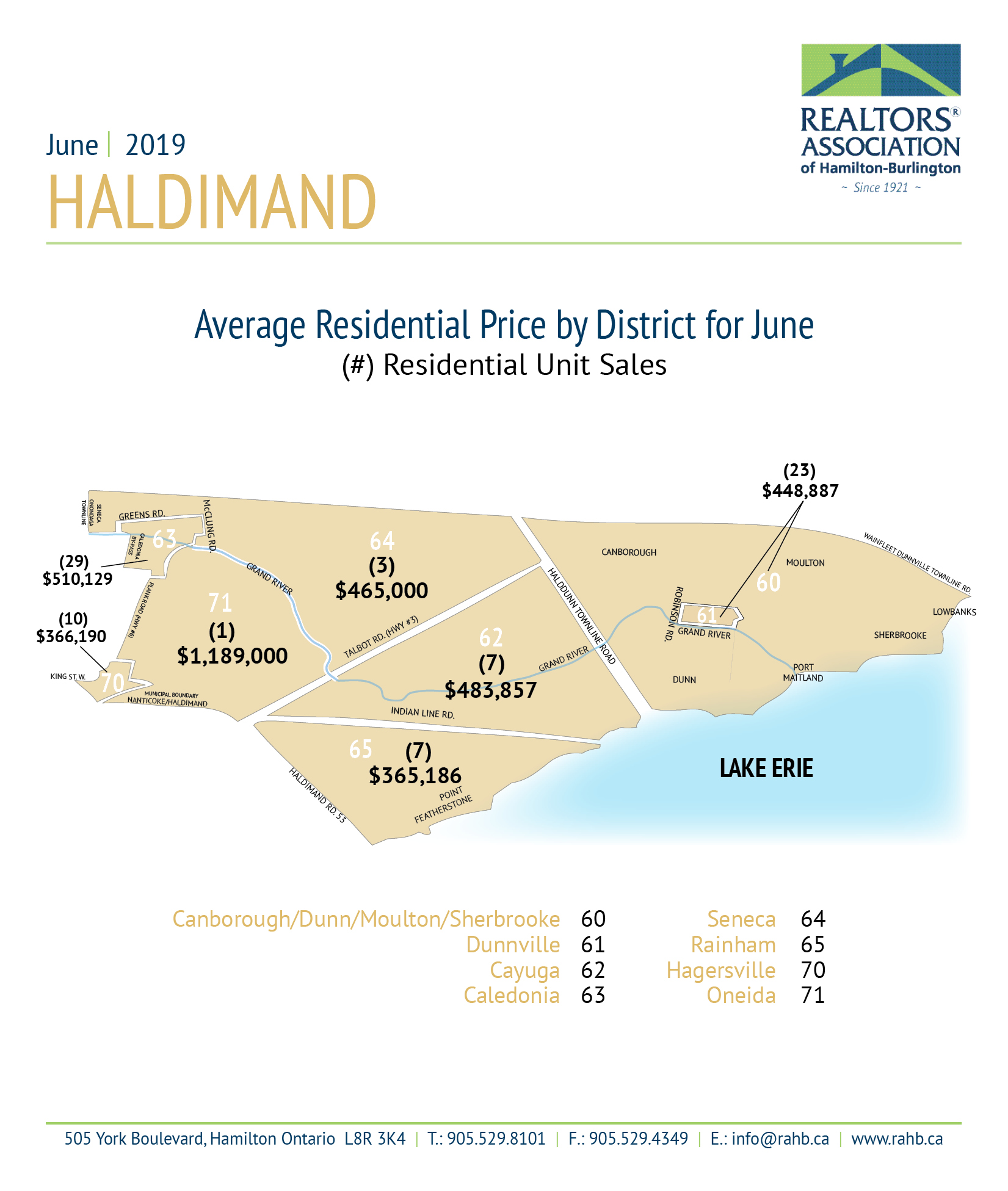

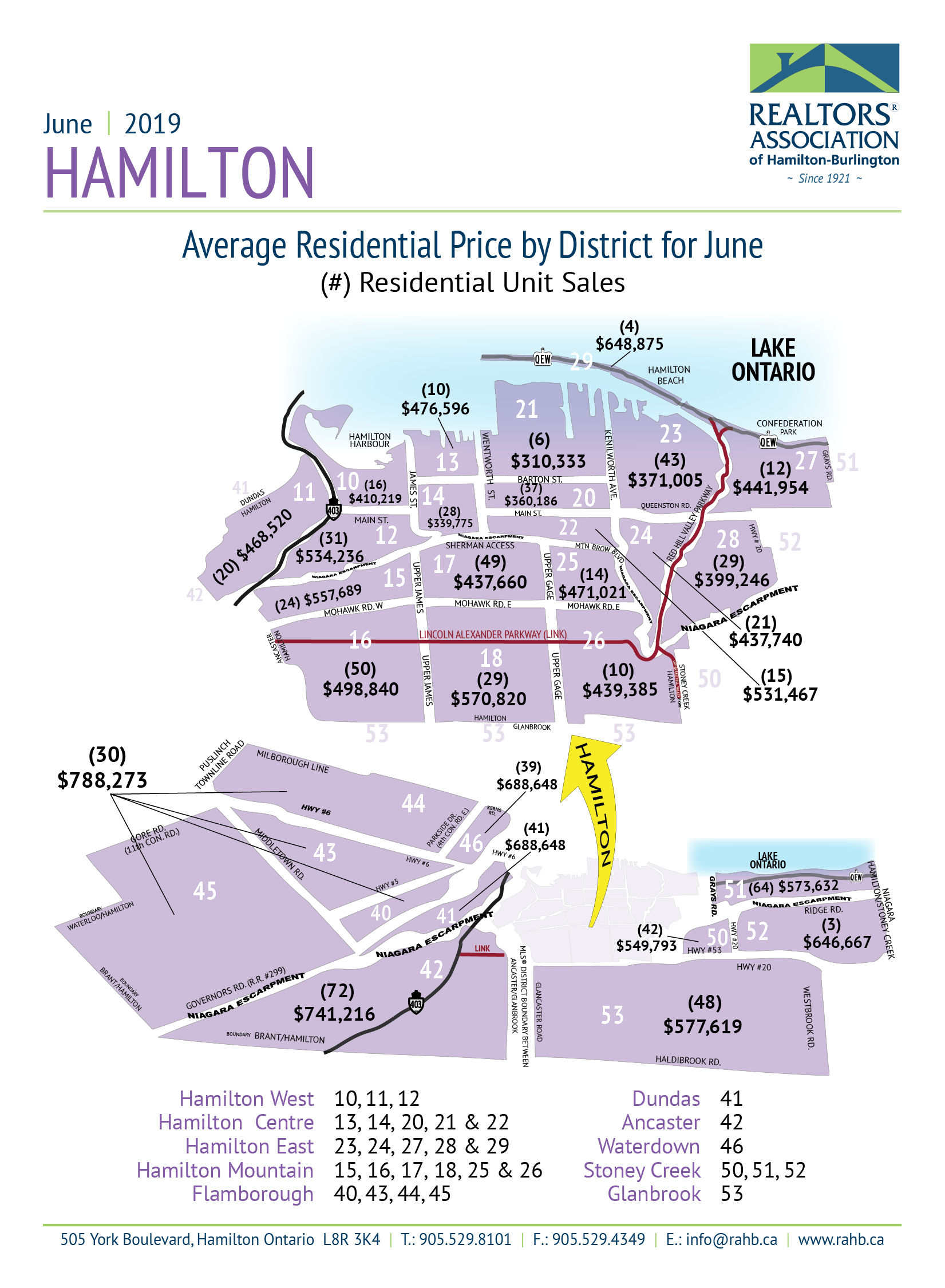

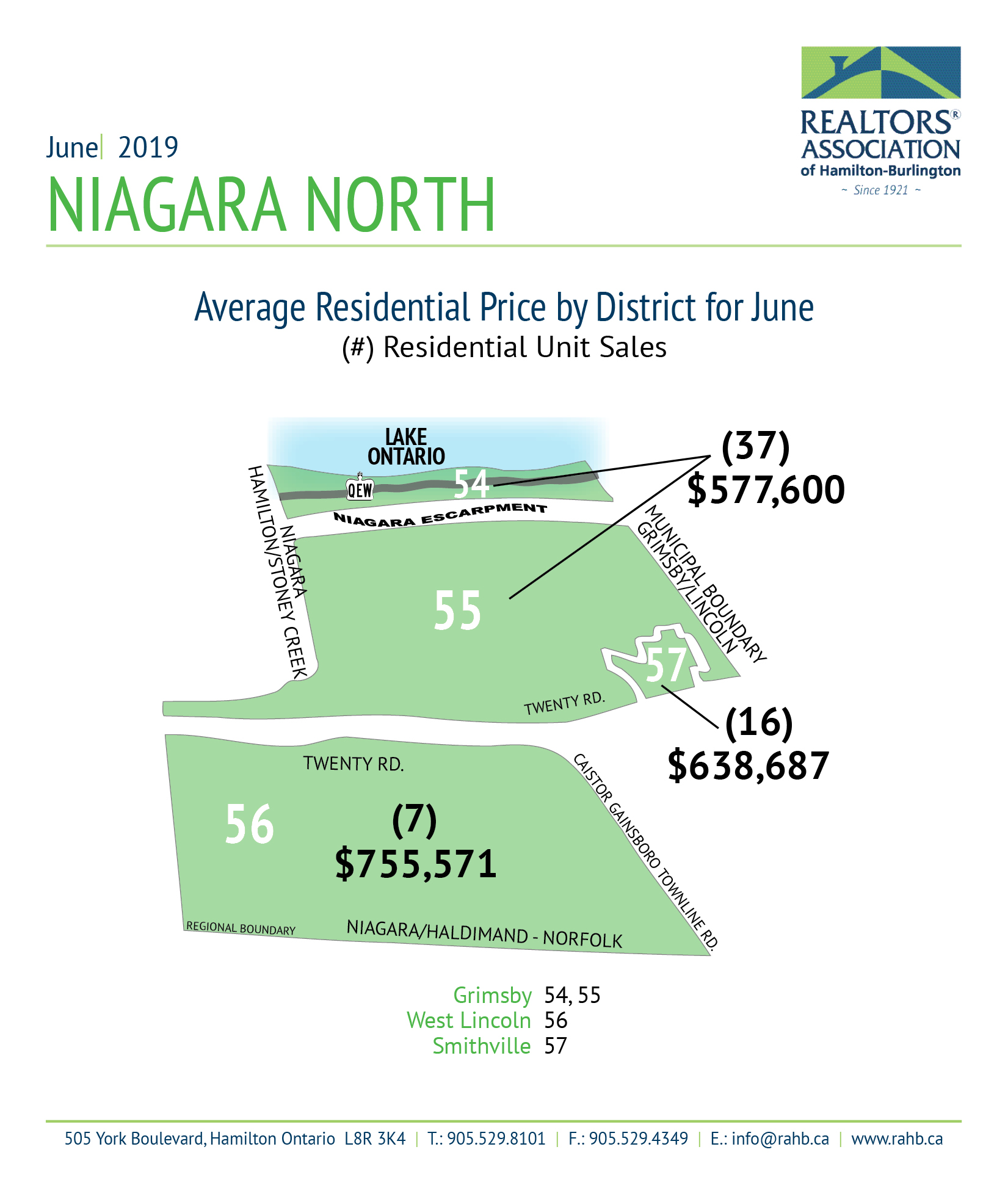

Hamilton, ON (July 2, 2019) – The REALTORS® Association of Hamilton-Burlington (RAHB) reported 1,203 sales of residential properties located within the RAHB market area were processed through the Multiple Listing Service® (MLS®) System in June 2019. This is a 4.2 per cent increase from June last year; however, a 10.5 per cent decrease over May 2019 and a 1.9 per cent decrease from April 2019. The average price for residential properties increased by 5.2 per cent from June 2018 to $593,549; however, decreased from May 2019 by 0.03 per cent.

With an aging population continuing to grow, there has become a growing need for REALTORS® to specialize in selling and buying senior homes. Although once called a niche, Ontario’s senior population is projected to double from 16.7% of the population to about 24.8% of the population by 2041, because of the growing number of seniors; senior home buying and selling are becoming standard practice.

Some of the service and systems that come with being a REALTOR® specialized in senior real estate are:

Extra Help and Guidance

Many seniors are living alone in their home and are unaware of the next steps. A REALTOR® trained to work with seniors will set up a free initial consultation to offer guidance about the home buying/selling process and will present all the option for the transition. Depending on the client, this may be one or more home visits to make sure that the client feels informed and comfortable.

Slower Pace

The home selling/buying process is complex, and many terms, ideas, and contracts are presented during the process. Senior home buyers/sellers benefit from a slower pace so they can feel relaxed and not rushed into a significant decision.

Contracts in Plain English

REALTOR® will make sure that they can sit down with the client with a form of the contract that has large print and written in layman’s terms. This further consultation will allow for any questions and concerns to be raised initially before the final signing.

Encouragement

Every client is different. Some may not wish for family members to be privy to the details of their real estate transactions, while others may want their family members to be highly involved. A good REALTOR® should also welcome and encourage what makes their client feel most comfortable.

Guidance

The decision to transition to another home is a significant decision, and there are many housing choices and options. A good REALTOR® should present all the possibilities, even those that will not generate them compensation such as retirement communities, assisted living, or long term care.

Special Rates for Professional Fees

There are many REALTOR® who have automatically discounted rates on commission for seniors, so there is no need to worry about the stress of negotiating a deal.

Supporting Professionals

The home selling/buying process involves many professionals, and it is essential that a REALTOR® can recommend a few that they know have a good reputation from working with them in the past. These professionals may include lawyers, inspectors, lenders, stagers, estate planners, insurance and financial advisors.

Senior real estate is becoming more than just a niche, but a standard practice. With this standard practice of senior real estate comes the growing importance of being certified in senior real estate:

SRES®- Senior Real Estate Specialist® Course

October 21 to 22, 2019: SRES® designation indicated you are qualified to address the needs of home buyers and sellers age 50+ and to approach them with the best options and information during the home buying/selling process.

RAHB will be offering this course to members and non-members through the Real Estate Institute of Canada. For more information, click the button below:

As our society continues to age, making sure the senior population is aware of their options will have a direct impact on society as a whole. Supporting senior housing will not just help seniors, but will have positive net effects on the entire population — especially first time home buyers.

It is important that REALTORS® are aware of the importance of senior housing support. Supporting senior housing is supporting a better community for all.

Home Sharing

Nearly two-thirds of Ontario residents are living in homes too big for their needs. Outside the GTA, 85% of seniors are living in homes too large. Subsequently, it is becoming more difficult for millennial to afford homes across Canada – especially in major cities.

Canada’s rents are rising while the amount of vacancies is shrinking. A growing number of the country’s seniors are living in homes too big, while young Canadians are being forced to living in apartments too expensive. One solution offered by the Ontario Government was to share the living space already built, to create mutual benefit – home sharing.

Home sharing is where the homeowner, usually a senior, offers reduced rent for a room in their home in exchange for small chores and companionship. The idea of home sharing is developing attention in small towns and cities across Canada.

“This is about more than sharing a house,” says Tonya Salomons, a social worker at the National Initiative for the Care of Elderly at the University of Toronto. Home sharing is a multi-benefit opportunity for generations to mingle and learn from one another, improve the health of isolated seniors, while also helping young people find affordable rent.

The most successful home sharing programs involve a process where matched candidates meet, have a trial stay and, if both agree, sign a clear contract outlining expectations and rules while living together.

For more information on Home Sharing, please click here.

The First Time Home Buyer Market

Most seniors are living in homes that are too large for their current needs and in communities that no longer support their desires. Tax breaks and other monetary support offered to seniors will allow them to downsize to a home more suitable to their current needs while still offering independent and safe living. Additionally, housing options that support their desire for independent living will free up housing for millennials who are attempting to purchase a home in a community they can grow with their family that are currently occupied by seniors.

Unfortunately, the home sweet home comes at a cost that may become unmanageable for seniors. Seniors who wish to stay in their home (or downsize to a smaller home) become unable because of income constraints.

It is important that REALTORS® are aware of the resources the Municipal, Provincial and Federal Governments offer for seniors who are still living in their own home. As a result, they have created multiple programs like tax assistant grants and hydro assistance.

Senior Homeowners’ Property Tax Grant

The Provincial Government is offering a program for low-income seniors who can be eligible for up to $500 back on their property taxes.

To be eligible, each of these has to be accurate:

Paid Ontario property tax during the year

Met either of the following income requirements:

You were single, divorced or widowed and earned less than $50,000

You were married or living common-law, and you and your spouse/common-law partner acquired a combined income of less than $60,000

Owned and occupied your principal residence

Were 64 years of age or older

Where a resident of Ontario.

The max grant amount of $500/year is adjusted based on net income:

Single, separated, divorced or widowed:

Less than $35,000 = $500

$35,000 less than, but not greater than $50,000 = a grant reduction of 33.3% of your income over $35,000

Married or common-law:

Less than $45,000 = $500

Greater than $45,000 = 33.3% reduction of your income over $45,000

Greater than $60,000 = Do not qualify

Only one person per couple can receive this grant

Click here for an online calculator to see how much money you could receive

A tax return needs to be filed to apply for this grant:

General income tax and benefit return

Report the amount of property tax that is paid on line 6112 on the ON-BEN application

The grant is paid 4-8 weeks after the Canada Revenue Agency notifies you of the notice of assessment and a direct deposit will follow

Tax Assistance Program

The City of Hamilton offers a tax assistance program based on age or income; full tax deferral or compassionate appeals.

The Tax Deferral Program includes:

Interest that is compounded annually (2019 rate = 5%)

Annual application is required

Application fee of $200 with a $100 annual renewal fee after initial application

The application needs to be filed before September of the application year

You and your spouse are 65 years and older of age by January 2019 and receive assistance payments under the Ontario Disability Support Program, under disability pay under the Guaranteed Income Supplement, or an amount paid under the CPP disability benefit

Your total combined income is less than $36,100

You occupy the residential property as your principal residence

You own the primary home for at least one year preceding the application date

Compassionate Appeal

Tax reduction due to extreme sickness or poverty

Extreme poverty: A Financial Statement needs to be provided with the application

Severe disease: Attending Physician’s Statement and a Financial Statement need to be provided with the application

The City of Hamilton accepts the sympathetic requests and submits them to the Assessment Review Board, or ARB on behalf of the party

Needs to be filed before February of the application year

ARB mails a Notice of Hearing once a year, which usually happens in April

Please click here for the application form for extreme poverty

Please click here for the application form for extreme sickness and click here for a Financial Statement

Older Adults Property Tax Deferral Program

If you are an older adult and a homeowner living in the Halton Region on a fixed income, you may qualify for the Older Adult Property Tax Deferral Program. The goal of the program is to help older residents on fixed incomes to manage the rising cost of living and remain in their homes.

To qualify for the program, you must be able to meet the following criteria:

You are at least 65 years old.

You own a home in Halton Region.

At least one registered owner must have lived in the home (as their principal residence) for the last four years.

Your combined pre-tax gross annual income (the applicant plus the property’s registered owners) must be less than $50,900.

You are not participating in any other property tax deferral or rebate programs.

You have paid your previous years’ property taxes in full.

The City of Burlington will review your eligibility for the program every year. Once deferral begins, you must submit a completed renewal by September 30 each year to stay in the program.

If you do not apply for renewal by September 30, or if you are no longer eligible for the program, The City of Burlington will continue to defer your property taxes for that year.

After this first year, you will have a one-year grace period to reapply and show your eligibility. The City of Burlington will continue to defer your taxes, interest-free, during this time.

If you reapply during the grace period and are eligible for the program, your property taxes will continue to be deferred.

Unless you end participation, such as by selling your home, the program provides two full years to renew your application and show your eligibility before you must repay the remaining deferred taxes.

Enrolment in the program includes the following fees:

Initial application fee of $50

One time administration fee of $200

Annual renewal application fee of $0

Please click here for the eligibility and calculator tool

Please click here for the renewal application form

Tax Rebate

Haldimand County offers seniors or low income disabled property owners a deferral of local taxes if specific criteria is met.

Click here to access the application for deferral of local taxes for low income seniors or low income disabled property owners and the specific criteria that needs to be met for collection of the deferral

Home Assistance Program

Hydro One offers free energy-efficient upgrades to the home.

To be eligible for the program you have to be a Hydro One customer and:

Own or rent your home or live in an eligible non-profit housing property

Your gross household income for the last year is not more than these income levels

1 Person

$32,843

2 People

$40,886

Or you have received one of the following in the past 12 months:

Allowance for the Survivor

Guaranteed Income Supplement

Allowance for Seniors

Ontario Works

Ontario Disability Support Program

Or you have received a Low-Income Energy Assistance Program Grant or were part of the Ontario Electricity Support Program in the past 12 months

Click here for more information on the Home Assistance Program

Ontario Electricity Support Program

The Ontario Electricity Support Program is offered by the Ontario Government that provides a monthly on-bill credit for lower-income customers to reduce their electricity bill.

Eligibility is based on the number of people living in the home and the total annual household income after taxes

Click here for a new application form and to see if you are eligible for the program.

Click here to renew an application for the program.

Budget Billing

A program offered through Hydro One where you pay the same amount each month to more efficiently manage your household budget.

How Budget Billing works:

Monthly budget billing is set based on your billing history to even out your energy cost over a year

Pay the same amount for six months, and on the six and nine months, your monthly payment amount is reassessed to make sure you are not paying too little or too much

Have to lock in for 12 months

These programs offered will help to reduce the stress associated with the cost of staying in the home. It is possible for seniors to afford to continue to live at home. As a result, RAHB has created infographics with the information above that can be given to a senior client or that senior’s family so that they are aware of all the affordability options available to seniors.

Please click the buttons below to access infographics that can be given to clients or their family on the information above:

On September 2, the Federal First-Time Home Buyer Incentive will be launched.

Under the plan, the government is attempting to help some first-time home buyers with:

Advancing an interest-free loan of up to 5% of the purchase price of an existing home and up to 10% of the cost of a new build

Increasing the amount first time home buyers can borrow from their RRSPs to now $35,000

However, to apply for the interest free loan, buyers must have a household income below $120,000 a year. Additionally, the total value of the mortgage plus the Canadian Mortgage and Housing Corporation portion does not eclipse $480,000.

For more information, please click the button below:

I know many of you are interested in the recruitment process for RAHB’s new CEO. Our CEO Selection Committee has reported that they’re on schedule and the position will be posted shortly.

The CEO Selection Committee has worked with a hiring company – Optimum Talent – to create a posting that I’m sure will generate a lot of interest. I know that the Committee is working very well together and I’m confident they will identify a great list of qualified candidates.

I would like to thank the interim CEOs – Kim and Carolyn – for providing great leadership during this time of transition. Staff morale is high and RAHB is continuing to function effectively and efficiently. We are fortunate to have dedicated and resilient staff members who are committed to providing great service to RAHB members.

At yesterday’s meeting the Board of Directors also heard an excellent presentation from ORTIS on their history as an organization and the services they offer to ORTIS members. With the announcement of ORTIS and the Ontario Collective (OC) agreeing to blend their MLS® Systems, we are considering all options with regards to our data-sharing arrangement with ORTIS. Both RAHB and ORTIS are unwavering in support of the principle of open access to MLS® data for all REALTORS®. They reassured us that RAHB data is extremely important to their members – just as their data is important to all of us.

Over the coming weeks I will keep you informed regarding the progress of both the CEO recruitment process and the ongoing data-sharing options/negotiations. We will also be issuing a survey to members to request your feedback regarding TREB – i.e. interboarding, TREBHomes, access to data, sales and listings, etc. So please keep an eye on your e-mail for that survey – the information collected will be very beneficial to make decisions moving forward.

This is an important and busy time for our organization. Thank you for your ongoing interest in RAHB’s activities and please don’t hesitate to contact me personally if you have questions or comments.

Congratulations Raptors – We the North!

Bob Van de Vrande, B.Comm., M.B.A., B.Ed.

2019 RAHB President

REALTORS® Association of Hamilton-Burlington

Attention RAHB members! Rental scams continue in Hamilton.

RAHB continues to receive reports from members who find their for-sale properties posted without permission for rent on various online classified websites.

If you see or are affected by a rental scam, Hamilton Police suggest reporting the ad to the website where the rental is posted, to local police services and to the Canadian Anti Fraud Centre at 1.888.495.8501.

We also recommend notifying RAHB so we can warn other RAHB members, as well as the public.

It is just as crucial for the administrative staff to understand and comply with the Real Estate and Business Brokers Act, 2002 (REBBA) as it is for the Broker of Record. Now, RECO’s Mandatory Continuing Education (MCE) allows registrants to be able to share course content with non-registrants, like the administrative staff.

Non-registrant staff can access A Guide to Brokerage Inspection by clicking the button below:

There is no place like home, and sometimes it seems like there is no place safer; however, the house is where many common injuries occur – like falling. Changes that are a part of the routine aging process, such as declining vision, hearing and bone density, can increase the risk of injuries. Injuries that were once minor become more seniors because as the body ages, it takes longer to recover from an injury.

The Government of Canada has created a guide called Safe Living Guide – A Guide to Home Safety for Seniors. This guide offers checklists to help inspect the home for evidence of hazardous areas that can cause injury.

Click the button below to download the checklist that can be given to a senior client or their family:

Sometimes, a senior client believes that selling their home is their only option when it becomes not as safe as it once was. However, there are many programs offered to seniors with mobility issues that will allow them not to have to sell their home.

Halton Accessibility Repair Program

Grants and loans are provided to improve the accessibility of home and promote independent living.

The following must be true to be eligible for a grant or loan:

You are the sole owner(s) of the house

You have not started home modifications

All members of your home are legal Canadian citizens

Household income is less than $92,200

The value of the property is less than $834,839

Your property tax, mortgage payments and home insurance (for the full amount of the property) are all paid up to date

Applications are based on a first come, first serve basis, and there is limited funding available. If you do not receive funding for the year you apply, you will be placed on a waitlist and receive funding when possible.

For more information on the Halton Accessibility Repair Program, click here.

Home and Vehicle Modification Program

Offered through March of Dimes Canada, provides funding for necessary home modification and is intended to assist permanent Ontario residents with a substantial impairment that is expected to last one year or more.

The following must be accurate to be eligible for a grant or loan:

You are a permanent Ontario resident

Ongoing or recurring disability/impairment that is anticipated to continue more than one year

Your disability/impairment impedes mobility and results in substantial restrictions in activities of daily life

It may be possible to qualify for up to $15,000 towards home modification:

If you have a gross annual income of over $35,000, you may be required to contribute towards the cost of the requested home modification(s)

If the applicant receive ODSP Income Support, Ontario Works, or the Old-Age Security Guaranteed Income Supplement as their only source of income, you are not required to complete the Financial Calculation Worksheet

For more information on the Home and Vehicle Modification Program, click here.

Exercise and Fall Prevention Programs

Seniors (65+) can join free classes to help maintain balance and strength to help prevent falls. A physiotherapist or other health professionals teach fall prevention classes and provide information on preventing falls for seniors.

There is no referral needed.

Click here for exercise and fall prevention programs in Hamilton, Niagara, Haldimand and Brant.

These programs, no matter how large or small the effect is, can help seniors live at home independently longer and will give ease to their family. A client will appreciate the concern REALTORS® have in regards to senior safety in their home.

Attention to all affordable housing stakeholders in the Halton Region!

Halton Region has released a new initiative that pertains to a Request for Applications (RFA) to receive Regional capital assistance in support of affordable housing development across the Region of Halton.

The purpose of the RFA is to identify and fund eligible rental housing projects using capital funding programs administered by the Region, specifically:

Increase the supply of purpose-built, affordable rental housing stock in Halton Region with easy access to a range of supports that may be needed for people to lead stable and independent lives.

Ensure this affordable housing stock is energy efficient, accessible and sustainable over the long term.

Support partnerships that allow for the creation of more affordable housing and affordable housing communities.

Work towards negotiated RFA outcomes in August 2019 for a potential award by the Regional Council in October, and subsequent construction starting in the spring of 2020.

If this sounds of interest to you, applications must be sent to The Office of the Manager of Purchasing and delivered to main reception at:

The Regional Municipality of Halton

1151 Bronte Road

Oakville, Ontario

L6M 3L1

Applications must be submitted by July 4, 2019, at 2 pm

You can download the application by clicking the button below:

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}